When it comes to financial planning, life insurance often occupies a pivotal role, yet it remains a topic shrouded in complexity and misunderstanding for many. Whether you are a seasoned planner or just beginning to explore your options, understanding life insurance is essential to securing your financial future and protecting your loved ones. In this article, we will delve into the fundamental aspects of life insurance, breaking down its various types, benefits, and crucial considerations that can help you make informed decisions. From dispelling common myths to highlighting key features and strategies, our goal is to equip you with the essential insights that empower you to navigate the world of life insurance with confidence.

Table of Contents

- Understanding the Different Types of Life Insurance Policies

- Key Factors That Affect Life Insurance Premiums

- The Importance of Regular Policy Reviews and Updates

- Navigating the Claims Process: Tips for a Smooth Experience

- In Summary

Understanding the Different Types of Life Insurance Policies

Life insurance comes in various forms, each designed to meet different financial needs and goals. The two primary categories of life insurance are term life and permanent life insurance. Term life insurance provides coverage for a specified period, typically ranging from 10 to 30 years. It’s often more affordable, making it a popular choice for young families or individuals who wish to cover short-term financial obligations like mortgage payments or education costs. Alternatively, permanent life insurance offers lifelong coverage and can build cash value over time, making it an attractive long-term financial tool. Common types of permanent life insurance include whole life, universal life, and variable life policies, each varying in terms of premiums, investment options, and death benefits.

To help you further understand these options, here’s a brief comparison of the different types of permanent life insurance:

| Type of Insurance | Key Features | Ideal For |

|---|---|---|

| Whole Life | Fixed premiums, guaranteed death benefit, cash value accumulation | Those seeking stability and predictable costs |

| Universal Life | Flexible premiums, adjustable death benefits, cash value based on interest rates | Individuals wanting more control over their policy |

| Variable Life | Investment options for cash value, death benefit may vary | People comfortable with investment risks and seeking growth |

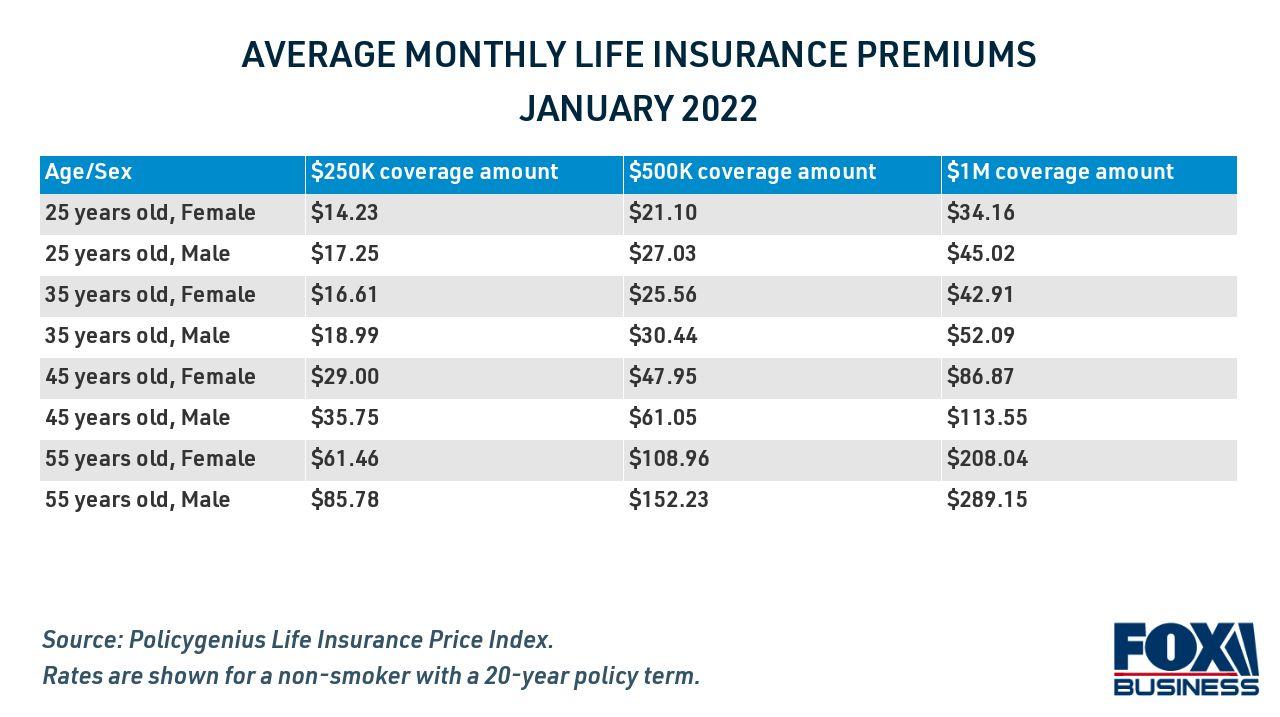

Key Factors That Affect Life Insurance Premiums

When determining life insurance premiums, several crucial elements come into play, each influencing the cost and coverage options available to you. Age is often the most significant factor, as younger individuals typically pay lower premiums due to their longer life expectancy. Health status is equally important; insurers will evaluate your medical history and any pre-existing conditions, as these can impact your lifespan and risk profile. Other contributing factors include your occupation, which may pose higher risks, and lifestyle choices, such as smoking or extreme sports, that can lead to increased premiums.

Moreover, individuals should consider their coverage amount and the type of policy they choose, whether it’s term or whole life insurance. The length of the policy duration also significantly affects pricing; longer terms often come with higher premiums due to extended coverage. For a clearer understanding of how these factors interact, here’s a simplified comparison of their potential impacts on premium rates:

| Factor | Impact on Premiums |

|---|---|

| Age | Lower rates for younger applicants |

| Health | Higher rates for poor health conditions |

| Occupation | Higher rates for risky jobs |

| Lifestyle Choices | Increased rates for smokers or risky activities |

| Coverage Amount | Higher premiums for more coverage |

The Importance of Regular Policy Reviews and Updates

Managing a life insurance policy is not a one-time affair; it requires ongoing attention and care. Regular policy reviews are essential to ensure that your coverage remains aligned with your evolving life circumstances. As your life changes—be it through marriage, the birth of a child, a new job, or even retirement—so too do your insurance needs. A periodic review can identify gaps in coverage or areas where you may be overinsured, allowing you to adjust your policy accordingly. This proactive approach helps in maximizing the benefits of your life insurance investment.

Furthermore, the insurance landscape is always changing due to new regulations, market conditions, and product innovations. Keeping your policy updated means that you can take advantage of any new offerings or enhancements that the insurer may have introduced. Consider the following factors during your review:

- Changes in your financial situation

- Updated beneficiaries

- Shifts in your health status

- Life events like divorce or retirement

Establishing a routine for these reviews, perhaps annually or bi-annually, can help you stay ahead and ensure that your policy remains beneficial for you and your loved ones.

Navigating the Claims Process: Tips for a Smooth Experience

Understanding the claims process can feel overwhelming, but with the right approach, it doesn’t have to be. Here are some essential tips to help you navigate this often-complex journey:

- Gather Necessary Documents: Ensure you have all required paperwork handy, including the insurance policy, death certificate, and any other relevant documentation. This will expedite the claims process.

- Contact Your Insurer Promptly: Notify the insurance company as soon as possible. Each insurer has specific timelines for claims, and timely communication can make a significant difference.

- Understand Your Policy: Familiarize yourself with the nuances of your life insurance policy, especially coverage limits and exclusions, to anticipate any potential questions.

- Keep Records: Document all interactions with the insurance company. Note who you spoke with, the date, and the details discussed, which can be invaluable if discrepancies arise.

Another effective strategy is to enlist the help of a qualified professional, such as a financial advisor or attorney, if you encounter difficulties. They can offer guidance tailored to your specific situation. To illustrate an overview of the claims timeline, consider the following table:

| Step | Timeframe |

|---|---|

| Notification of Claim | Within 30 days |

| Document Submission | As soon as possible |

| Claim Review Process | 1-2 weeks |

| Claims Decision | Within 30 days of all documents received |

By being proactive and organized, you can simplify the claims process significantly, helping to ensure a smoother experience during what can be an emotionally challenging time.

In Summary

understanding the nuances of life insurance is crucial for making informed decisions that can impact your financial security and peace of mind. Whether you’re exploring different policy types, assessing your coverage needs, or staying informed about industry changes, the insights shared in this article serve as a foundation for navigating the complexities of life insurance. Remember, it’s not just about protecting your loved ones; it’s also about safeguarding your financial legacy. As you embark on this journey, consider consulting with a licensed insurance professional who can provide personalized guidance tailored to your unique situation. Armed with knowledge and the right resources, you can confidently approach life insurance and ensure that you are taking the necessary steps to protect what matters most. Thank you for reading, and here’s to securing a safer future for you and your loved ones.