In an unpredictable world where life often takes unexpected turns, financial security becomes a cornerstone for peace of mind. While many people diligently save for retirement and invest in their future, one crucial aspect often overlooked is the protection against unforeseen disabilities. Disability insurance serves as a safety net, providing essential financial support when illness or injury prevents you from working. In this article, we will explore why disability insurance is vital for maintaining financial stability, how it works, and the various options available to help safeguard your income. Whether you’re just starting your career or are well-established in your professional life, understanding the importance of disability insurance can empower you to make informed decisions for your future.

Table of Contents

- The Importance of Disability Insurance for Income Protection

- Understanding the Types of Disability Insurance Available

- Evaluating Your Coverage Needs for Comprehensive Financial Security

- How to Choose the Right Disability Insurance Policy for Your Lifestyle

- Closing Remarks

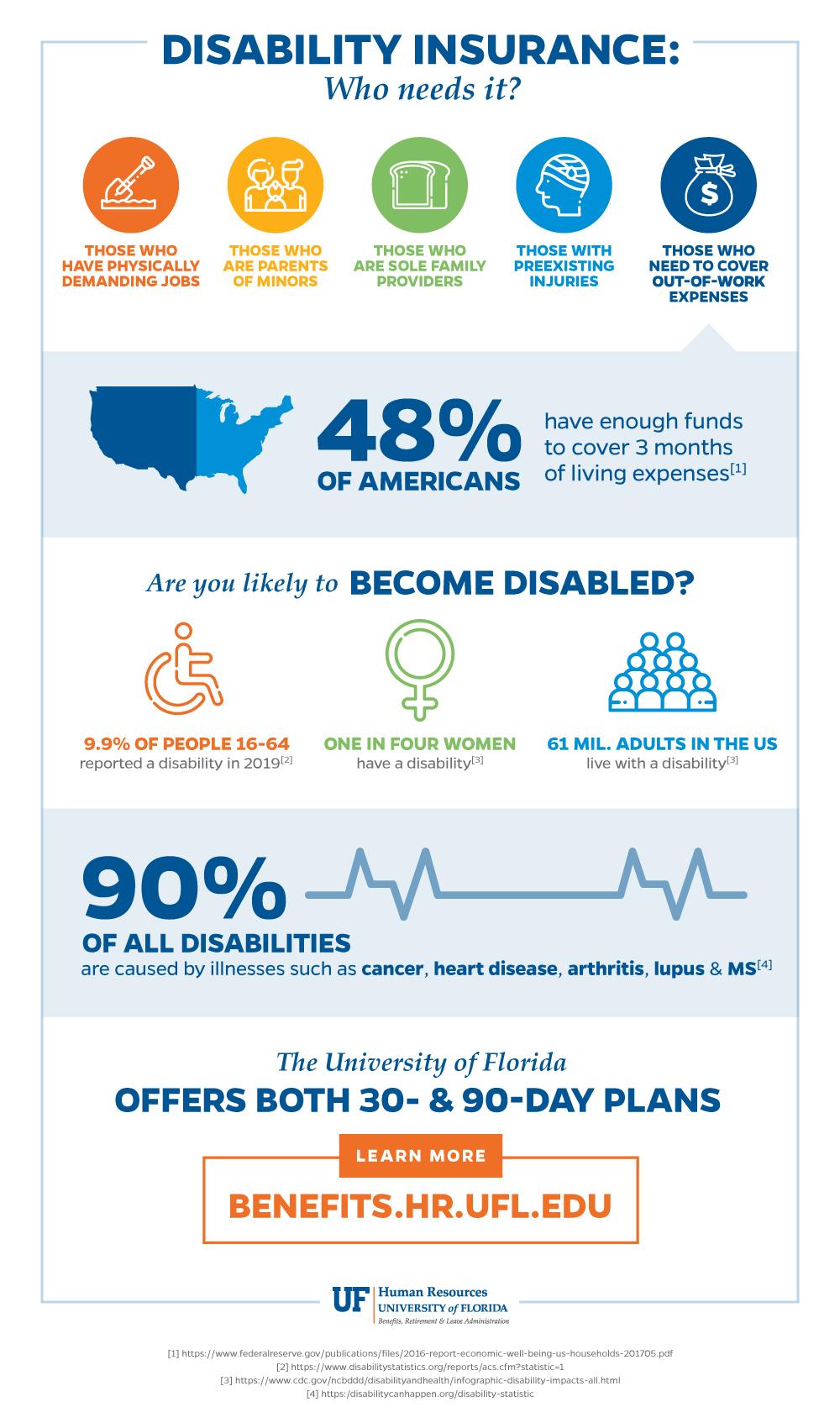

The Importance of Disability Insurance for Income Protection

For many individuals, the unexpected can become a harsh reality. A sudden illness or injury can incapacitate a person and hinder their ability to earn a living. Disability insurance serves as a crucial financial safety net in these times, ensuring that even when life takes an unexpected turn, your income remains protected. Without such coverage, individuals may struggle to pay daily expenses, medical bills, or maintain their quality of life. This financial strain can lead to long-term implications, including depletion of savings and increased stress. Investing in disability insurance means investing in your peace of mind.

Moreover, the advantages of disability insurance extend beyond mere income replacement. It allows individuals to focus on recovery rather than financial turmoil. Here are a few key benefits of having disability insurance:

- Continued income: Replaces a portion of your salary, easing financial burdens.

- Access to funds: Ensures you can cover ongoing expenses like rent, utilities, and groceries.

- Specialized care: Enables you to afford necessary medical treatments or rehabilitation.

As you evaluate your financial strategy, consider incorporating disability insurance into your plan to safeguard your future. Below is a simple comparison of different types of disability insurance:

| Type of Insurance | Coverage Duration | Typical Benefit Percentage |

|---|---|---|

| Short-term Disability | Up to 6 months | 60-70% |

| Long-term Disability | More than 6 months | 50-70% |

| Social Security Disability | Varies | Varies |

Understanding the Types of Disability Insurance Available

When considering disability insurance, it is essential to understand the various types available to find the best fit for your needs. There are primarily two main categories of disability insurance: short-term and long-term. Short-term disability insurance provides coverage for a limited duration, typically ranging from a few months up to a year, and is designed to replace a portion of your income during that period if you are unable to work due to illness or injury. On the other hand, long-term disability insurance kicks in after short-term coverage ends and can last for several years or even until retirement, depending on the policy. This type of insurance is crucial for ensuring long-lasting financial protection during extended periods of incapacitation.

Furthermore, disability insurance policies can vary significantly in terms of their definitions of disability and coverage specifics. Some policies offer a “own-occupation” definition, which means you’ll receive benefits if you can’t perform the specific duties of your job, while others might follow an “any occupation” definition, which implies that you won’t be eligible for benefits if you can work in any job, even if it’s not in your previous field. Additionally, riders can be added to enhance coverage, such as cost-of-living adjustments or waiver of premium, ensuring your policy remains robust amidst inflation or financial strain. Understanding these variations is crucial to making an informed decision that secures your financial future.

Evaluating Your Coverage Needs for Comprehensive Financial Security

Understanding your coverage needs is essential for achieving comprehensive financial security, particularly when it comes to disability insurance. Many individuals underestimate the impact that a disabling condition can have on their ability to earn an income. Disability insurance serves as a safety net, providing you with a percentage of your income during periods when you are unable to work due to illness or injury. When evaluating the right level of coverage, consider factors such as your current expenses, savings, and other sources of income, as these elements will guide you in determining how much coverage you truly need.

To effectively tailor your disability insurance plan, it’s helpful to assess various components holistically. Here are some key criteria to consider:

- Income Level: Calculate how much income you would need to maintain your current lifestyle.

- Duration of Coverage: Assess how long you would require benefits, factoring in both short-term and long-term needs.

- Existing Assets: Evaluate your savings and other assets that can support you during periods of disability.

- Healthcare Costs: Anticipate potential medical expenses that may arise alongside your disability.

Additionally, it’s wise to review your existing policies to identify gaps or overlaps in coverage. The following table summarizes the different types of disability insurance available:

| Type of Disability Insurance | Description | Ideal For |

|---|---|---|

| Short-Term Disability | Covers a portion of income for a limited time, typically up to 6 months. | Temporary conditions, recovery from surgery. |

| Long-Term Disability | Covers a portion of income for extended periods, often until retirement age. | Major disabilities, chronic health issues. |

| Own Occupation Coverage | Provides benefits if you’re unable to perform your specific job. | Specialized professions with unique skill sets. |

| Any Occupation Coverage | Benefits are paid if you can’t perform any job for which you’re reasonably suited. | General coverage for broader safety. |

How to Choose the Right Disability Insurance Policy for Your Lifestyle

When selecting a disability insurance policy, it’s crucial to assess your personal and professional lifestyle. Start by evaluating your current income and expenses to determine how much coverage you need to maintain your standard of living. Consider factors such as:

- Your occupation: Certain jobs carry higher risks of injury or illness, influencing the type of coverage you may require.

- Your health history: Pre-existing conditions can impact policy options and premium costs.

- Family responsibilities: Dependents relying on your income might necessitate more extensive coverage.

Another significant aspect is understanding the policy’s details, including the waiting period before benefits kick in and the duration of these benefits. To simplify your decision-making, you might find it helpful to compare quotes from multiple providers. Creating a comparison table can make this process easier:

| Provider | Monthly Premium | Benefit Period | Waiting Period |

|---|---|---|---|

| Provider A | $120 | 5 years | 30 days |

| Provider B | $150 | 2 years | 60 days |

| Provider C | $100 | 10 years | 90 days |

By closely examining these features against your needs, you can identify a policy that not only aligns with your financial goals but also provides reassurance in the face of unexpected life changes.

Closing Remarks

disability insurance is a critical component of a comprehensive financial security plan. It provides peace of mind and a safety net during uncertain times, ensuring that you and your loved ones can maintain your standard of living even if the unexpected occurs. By investing in disability insurance, you are not only protecting your income but also safeguarding your future and enabling a sense of stability amidst life’s challenges. Remember, taking proactive steps today can make all the difference tomorrow. Whether you’re just starting your career or are well into it, consider evaluating your options and determining the right coverage for your unique needs. After all, financial security is not just about wealth accumulation; it’s also about being prepared for life’s unpredictability.