When it comes to insurance, misinformation and myths abound, leading many to make ill-informed decisions about coverage. From common beliefs about premiums to misconceptions about what policies actually cover, these myths can result in financial pitfalls and unmet expectations. In this article, we aim to debunk some of the most prevalent insurance myths and provide you with the facts you truly need to know. Whether you’re navigating health, auto, home, or life insurance, understanding the realities behind these myths can empower you to make better choices and secure the coverage that best fits your needs. Let’s separate fact from fiction and help you better navigate the often confusing world of insurance.

Table of Contents

- Understanding the Misconceptions Surrounding Coverage Types

- Clarifying the Role of Deductibles and Premiums

- Exploring the Truth About Claims and Payouts

- Common Beliefs About Bundling Policies and Discounts

- In Conclusion

Understanding the Misconceptions Surrounding Coverage Types

Insurance can often seem like a minefield of jargon and confusion, leading many to develop misconceptions about different types of coverage. One of the most prevalent myths is that all insurance policies are essentially the same. In reality, coverage types vary significantly based on specific needs and circumstances. For instance, while homeowners insurance protects your property and personal belongings, renter’s insurance is designed for those who do not own their living space, offering protection for personal possessions instead. Understanding the nuances between these coverages can help individuals choose the right policy for their unique situations.

Another common misconception is that lower premiums mean less coverage, which isn’t necessarily true. Many people believe that opting for a basic policy will leave them underinsured, but this isn’t always the case. It’s essential to analyze the coverage limits and deductibles of a policy rather than just focusing on the premium cost. To illustrate this point, consider the following table highlighting essential aspects of different policies:

| Policy Type | Typical Premiums | Key Coverage |

|---|---|---|

| Homeowners Insurance | Medium to High | Property, Liability |

| Renter’s Insurance | Low to Medium | Personal Property |

| Auto Insurance | Medium | Liability, Collision |

By demystifying these common misconceptions, individuals can make more informed decisions when it comes to their insurance needs, ensuring they have the right coverage without overpaying for unnecessary extras. Understanding the distinct features of each type of coverage allows for better financial planning in the long run.

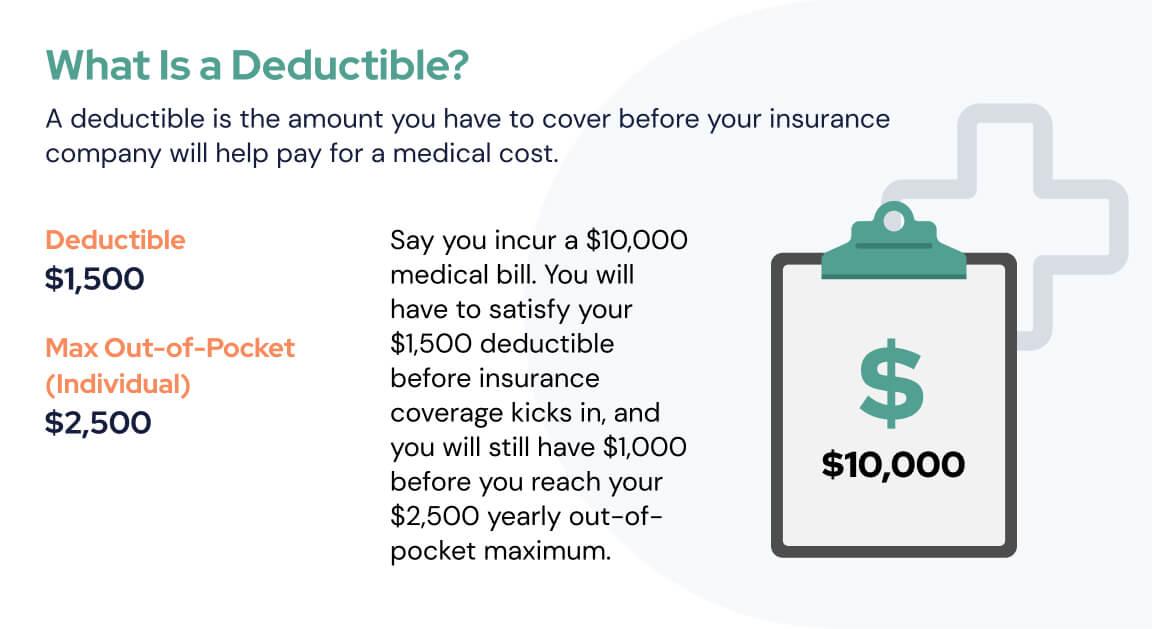

Clarifying the Role of Deductibles and Premiums

Understanding the financial mechanics of insurance can be daunting, but clarifying the roles of deductibles and premiums is essential for making informed decisions. Premiums are the payments you make, either monthly or annually, to maintain your insurance coverage. Think of them as an ongoing subscription to safeguard against unforeseen events. On the other hand, deductibles are the amounts you must pay out-of-pocket before your insurance kicks in. This means if you have a deductible of $1,000, you’ll need to cover that cost yourself before your insurer starts footing the bill for any claims.

To further illustrate how these two elements interact, consider the following key points:

- Higher Premiums, Lower Deductibles: Often, plans with higher monthly premiums come with lower deductibles, providing better immediate coverage.

- Lower Premiums, Higher Deductibles: Conversely, a lower premium plan may have a higher deductible, meaning you’ll pay more out-of-pocket in the event of a claim.

- Budget Considerations: Always assess your budget and potential health or property risks when selecting a combination of premiums and deductibles.

| Plan Type | Monthly Premium | Deductible |

|---|---|---|

| Basic Plan | $200 | $1,500 |

| Standard Plan | $300 | $750 |

| Comprehensive Plan | $400 | $250 |

Understanding these factors not only helps in choosing the right plan but also prepares you for visits to the doctor or unexpected repairs. Insurance may seem overwhelming at first, but getting to know your premiums and deductibles can empower you, making it easier to navigate the complexities of coverage.

Exploring the Truth About Claims and Payouts

When it comes to insurance, many people harbor misconceptions about how claims and payouts really function. One of the most prevalent beliefs is that once you file a claim, insurers automatically approve it without scrutiny. In reality, claims undergo a thorough investigation to verify their legitimacy. Factors influencing the approval process include documented evidence, policy terms, and the nature of the incident. Understanding this can help policyholders set realistic expectations and prepare their claims accordingly.

Moreover, the idea that insurers are constantly looking for ways to deny claims is another myth that needs to be debunked. Insurers are motivated to honor valid claims, as it is crucial for maintaining their reputation and customer trust. The payout process can sometimes lead to confusion, especially when terms like deductibles and coverage limits come into play. To clarify, here’s a simple breakdown of what typically impacts payout amounts:

| Factor | Impact on Payout |

|---|---|

| Deductibles | Amount deducted from payout; lowers total claim value. |

| Coverage Limits | Maximum payout allowed by the policy; caps reimbursement. |

| Claim Type | Different policies may cover different types of claims. |

Understanding these key components helps demystify the claims process and empowers policyholders to navigate their insurance needs with confidence. Staying informed and prepared is the best way to ensure you receive timely and fair compensation when it matters most.

Common Beliefs About Bundling Policies and Discounts

Many people believe that bundling insurance policies is the only way to secure significant discounts. While it’s true that bundling can lead to savings, it’s not a universal rule. Some insurers offer competitive rates on individual policies that may rival those of bundled options. Additionally, consumers can save by shopping around and comparing different insurance providers, as discounts and pricing structures vary widely. It’s essential to evaluate all available options rather than assuming that bundling is the sole path to financial relief.

Another prevalent myth is that once a customer bundles their policies, they lose the ability to negotiate rates in the future. This is misleading; many insurance companies encourage customers to reassess their policies regularly and adjust coverage to fit changing needs and circumstances. By maintaining an open line of communication with their insurer, policyholders can potentially negotiate better terms, whether they are bundled or standalone policies. Understanding that coverage should adapt over time empowers consumers to make informed decisions that align with their financial and personal situations.

In Conclusion

debunking insurance myths is essential for making informed decisions about your coverage and securing your financial future. By understanding the realities versus the misconceptions surrounding insurance, you can navigate the complexities of policies more confidently. Remember, whether it’s dissecting the fine print or clarifying coverage details, staying well-informed is the key. Don’t hesitate to consult with professionals if you’re ever in doubt—education is your best ally in the world of insurance. We hope this article has helped illuminate some common misconceptions and armed you with the knowledge you need to take charge of your insurance decisions. Stay safe, stay informed, and remember—truth is your best policy!